Light & Wonder has started 2025 with steady revenue growth, achieving a 2% year-over-year increase in total revenue for the first quarter, reaching $774 million. This marks the 16th consecutive quarter of year-over-year revenue growth, thanks to the robust performance of its gaming and iGaming divisions.

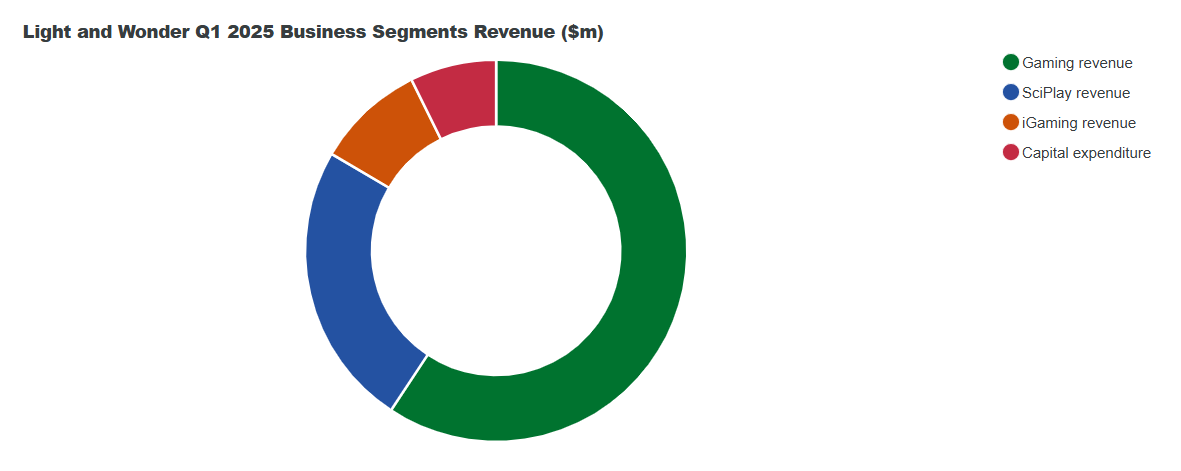

Gaming revenue grew by 4%, reaching $495 million, driven by growth across all segments. Table products sales increased by 9%, and gaming systems and operations revenue both grew by 5%.

The company saw a 30% increase in gaming machine shipments in North America and maintained its largest shipment volume share in Australia. Adjusted EBITDA for the gaming sector grew by 9%, reaching AU$254 million, with a profit margin increase of 200 basis points, reaching 51%.

Meanwhile, SciPlay's revenue decreased by 2% to $202 million, due to a decline in the average monthly paying users of its "Jackpot Party" game. However, the average monthly revenue per paying user (AMRPPU) rose to $116.96 million, driving EBITDA growth by 3% to $64 million, with a profit margin increase of 200 basis points to 32%. Direct-to-consumer sales contributed 13% of SciPlay's revenue.

iGaming revenue increased by 4%, reaching $77 million, with a record $25.2 billion in bets processed through the platform. The division's EBITDA grew by 8%, reaching $27 million, with a profit margin increase of 100 basis points. Growth was primarily driven by strong performance in the North American market and an expanding partner network.

Robust cash flow and strategic spending enhance long-term prospects

The group's adjusted EBITDA grew by 11%, reaching AU$311 million, reflecting improved profit margins across all three business divisions. Net profit remained stable at AU$82 million, with diluted earnings per share growing by 7%, to AU$0.94.

Adjusted NPATA also rose by 11%, reaching $117 million, with free cash flow growing by 19% to $111 million, driven by strong earnings and reduced capital expenditures.

Despite increased income tax expenses, operating cash flow climbed from $171 million in the same period last year to $185 million. Capital expenditures slightly decreased from $66 million in the first quarter of 2024 to $61 million this quarter.

The company returned $166 million to shareholders this quarter, repurchasing 1.9 million shares. Net debt stood at $3.9 billion, equivalent to a leverage ratio of 3.0 times, within the target range of 2.5 to 3.5 times.

Grover Gaming transaction and trade tariffs in focus

Light & Wonder has spent $850 million to acquire Grover Gaming's charitable gaming business, with the transaction expected to close in the second quarter. The deal was announced in February and is expected to expand L&W's operations in five regulated states in the US. Financing will come from a new $800 million term loan A credit facility.

The company also confirmed that it is mitigating potential cost pressures from new trade tariffs set to take effect in April 2025. Strategies under evaluation include supplier diversification and operational efficiency to offset expected increases in raw materials and component costs.

Past performance and market trends

Prior to the latest earnings release, Light & Wonder reached a new historical high. Total revenue for 2024 reached $3.2 billion, a 10% increase year-over-year. The gaming division led with a 12% increase, while iGaming and SciPlay grew by 9% and 6%, respectively. Net profit for 2024 jumped by 86.7%, reaching $336 million. Additionally, the company repurchased $462 million worth of shares in 2024, including $243 million in the fourth quarter alone.

Looking ahead, Light & Wonder reaffirms its adjusted EBITDA target of $1.4 billion for the full year of 2025 (pre-Grover transaction), and will host an Investor Day in New York on May 20 to provide further updates on its strategy and growth plans.